Occupancy Overview  2015 Strong Across the Senior Housing Spectrum

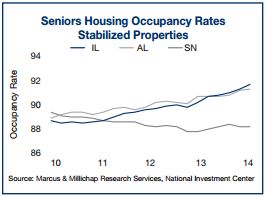

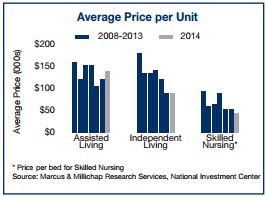

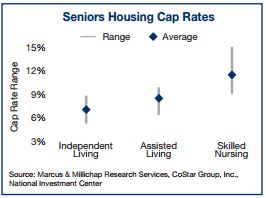

Every sector of the seniors housing market has positive momentum entering 2015 as the national economic picture brightens and demographic trends favor strengthening demand. Much of the ambiguity that faced the sector over the past few years has dissipated, though some of those factors may resurface in the years ahead. Currently, however, strong job growth across nearly every state is refilling local coffers and relieving pressure on state-funded reimbursements. Additionally, more questions surrounding the implementation of the Affordable Care Act and how it will impact operators have been answered, enabling owners to navigate the new system. The housing market is another bright spot for the industry. After the housing downturn, many seniors elected to stay in their homes rather than liquidate the largest chunk of their nest egg at rock bottom prices. Subsequently, robust appreciation supported a longer hold for those attempting to ride the market up again. Now that some normalcy has returned to the housing market for the first time in many years, a wave of seniors are financially and psychologically in a position to transition into some form of seniors housing. Similar to other real estate sectors, investors intend on expanding their portfolios this year while interest rates remain relatively low and the clouds that hung over the fate of reimbursements have begun to clear. In the independent living arena, intense demand for apartments is spilling into the sector as buyers outnumber sellers by a wide margin. The added spread between cap rates and interest rates for these properties has been a strong selling point for investors. Assisted living facilities, which typically do not receive the same level of interest from traditional multifamily buyers, are receiving a wave of new capital from REITs expanding in the sector. Approximately $30 billion in non-traded REIT funds could enter the seniors housing market this year, with a significant share targeted at private-pay assisted living facilities. On the other hand, the skilled nursing sector is poised for a renaissance of smaller operators in 2015. Uncertainty took a toll on deal flow at the lower end of the quality spectrum the past few years, and the current bright outlook could help investors recoup lost time. - source:Marcus & Millichap Comments are closed.

|