Senior Housing Sector Experiences Record-Setting Year

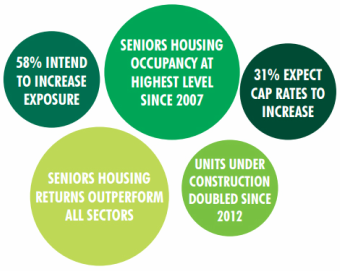

Senior housing occupancy is at its highest level since 2007, and 2015 was a record year for sales and institutional transactions, according to the recently released CBRE Senior Housing Investor Survey & Market Outlook. “Our survey was sent to the most influential senior housing investors, developers and brokers throughout the U.S.,” said Zach Bowyer, MAI, National Practice Leader for CBRE’s seniors housing specialty practice. “In developing the survey, our objective was to identify key trends in the senior housing real estate industry and to share this information with our clients to help them better understand the state of the rapidly evolving senior housing and care market.” The senior housing sector closed another record-setting year in 2015 with 514 institutional transactions closed and $18.7 billion in institutional sales, despite a slowdown in the fourth quarter, according to data from the National Investment Center for the Seniors Housing & Care Industry (NIC). The increase in volume over 2014 was 4.5 percent, revealing a significant decrease in growth rate, a trend that is consistent with the overall U.S. commercial real estate market. Among the key findings from the survey, 48 percent of respondents expect no change in cap rates over the next 12-month period. While 31 percent expect an increase in cap rates, 21 percent of the respondents are still expecting to see compression. The change in capitalization rates in 2015 was minimal compared to prior survey results, signaling that the market cycle is close to reaching a peak. Investor interest (old and new) remains high with 58 percent of respondents looking to increase their exposure to the space, while participation by public REITs in 2016 is a significant, yet unknown variable. Senior housing cap rates have averaged at a spread of roughly 518 basis points (bps) to the 10-year Treasury with the most recent indicated spread falling above the historical average at 554 bps. This indicates room for further compression as interest rates creep upward, according to CBRE. As a point of reference, multifamily cap rates currently represent a 215 bps spread.Total senior housing returns were reported at 16.3 percent, 14.8 percent and 13.3 percent over a one-, five- and 10-year period. These returns have outperformed multifamily returns and the NCREIF Property Index over the same periods. The number of units under construction has increased from 22,975 at the end of 2012 to 48,903 as of 4Q 2015. With an average development period of 12 to 15 months, a significant portion of this supply will come on line in 2016. This is a major concern in the industry. “The senior housing landscape is evolving with the increased presence of sophisticated capital, market transparency, operational efficiencies and technological advances. This can be compared to the institutionalization that the multifamily sector experienced from the mid-1990s to early 2000s,” said Mr. Bowyer. “Increased investment activity, coupled with increased construction activity, has resulted in an increased demand for experienced operators. Growing pains are expected as the market expands, and property management continues to be a key factor in protecting the value of a seniors housing asset.” For a copy of the CBRE Senior Housing Investor Survey & Market Outlook click here. |